VA Home Loans

WE GIVE 100% TO OUR VETERANS

We are dead serious about taking care of our veterans and service members. It’s an honor to be able to assist military families each year. For those who have sacrificed so much for our country, we are indebted to provide a second-to-none service.

VETERANS ARE EXPLOITED

VA homeowners are by far the most ‘ripped off’ sector of the lending industry, we have your 6. False advertising and misleading information is rampant. We are committed to giving each veteran or service member truth & insight.

VA INSIGHT

We are here to give you the whole truth about VA home financing. Access our VA Home Loan Series we created just for you.

VA BENEFITS SERIES

Get an inside look at recent seminar with bite-sized bits. This covers all general information on VA Home Loans.

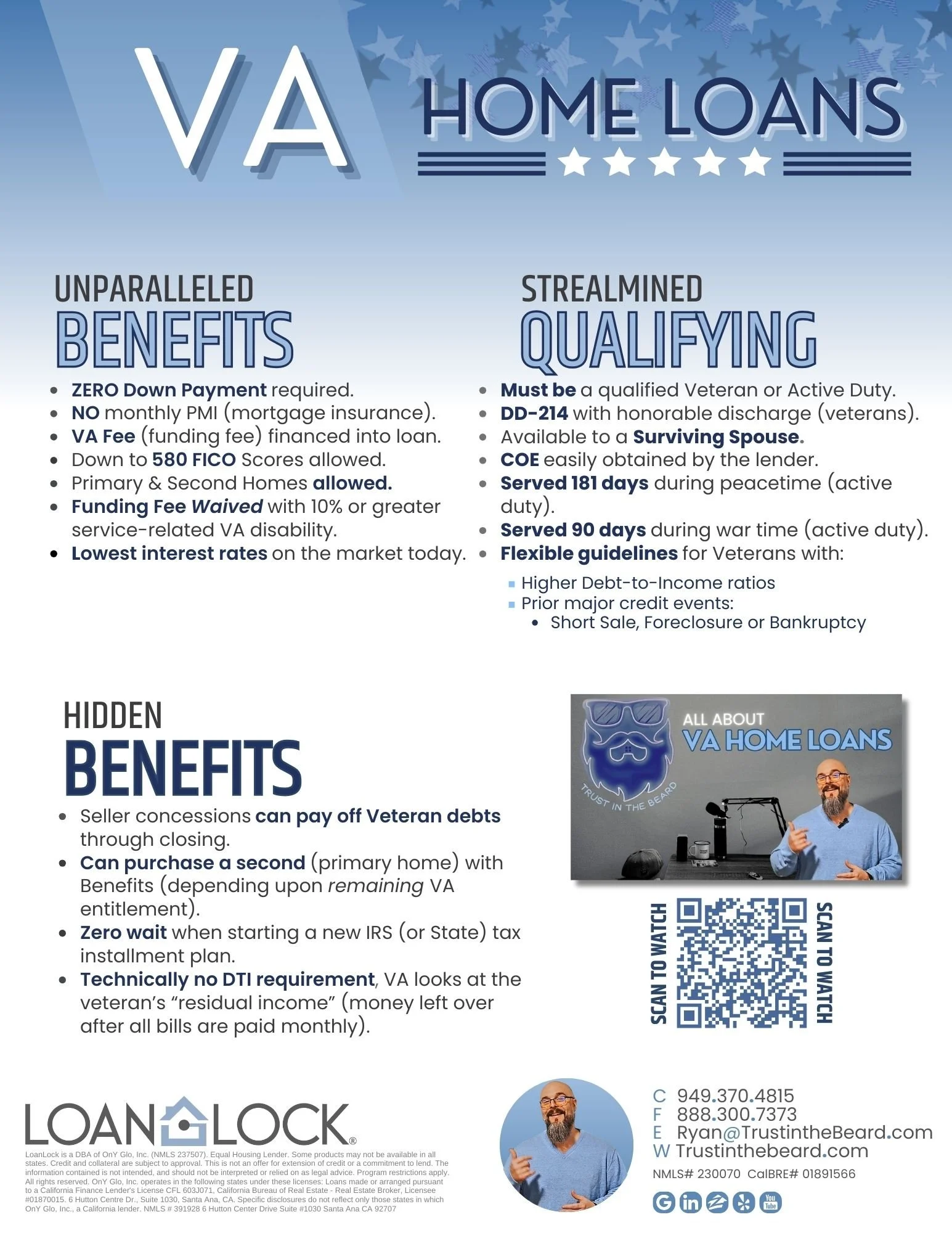

VA HOME LOAN FLYER

Check out the benefits, qualifying details and other hidden benefits of VA Home Loans.

VA BENEFITS

Payment

VA home loan benefits do not require a down payment.

0% Down

EVER

Save thousands of dollars not paying a monthly PMI.

No PMI

Employment History

You only need six months, sometimes less.

6 Months

Lenient Guidelines

VA guidelines are flexible with credit scores & history.

Low FICO

We Know VA Benefits

Some lenders claim to “specialize” in VA Financing. Believe it or not, we beat them in rates, service and knowledge

Commitment

We’ll do whatever it takes, even if that means cutting my beard. Seriously, our word and reputation is everything.

Transparency

We put everything on the table. Your in-depth consultation includes a screen share, you’ll see what we see!

Personal Approach

We will custom tailor a plan for each veteran, as no two clients have the same needs or goals.

Education

Where most lenders throw industry jargon and numbers at you, we speak in normal terms anyone can understand.

In-Depth Review

This is where we separate from the rest of our industry. Your consultation will leave you confident to make decisions.

Basic Entitlement Qualifications.

[01] ACTIVE OR RETIRED VETS

2 years of continuous active duty If discharged, must have been discharged “Under Honorable Conditions”.

[02] SURVIVING SPOUSE

Surviving Spouses may be entitled, if at least one of the below is true for the Veteran…

Is missing in action, or

Is a prisoner of war (POW), or

Died while in service from a service-connected disability and didn’t remarry, or

Died while in service from a service-connected disability and didn’t remarry before you were 57 years old or before December 16, 2003, or

Veteran had been totally disabled and died, but their disability may not have been the cause of death.

[03] RESERVES

6 years of combined service in the Selected Reserves or National Guard. If discharged must have at least an “Honorable” discharge. It is important to note that Reservist/National Guard boot camp does count towards the 6 year requirement.

[04] ACTIVE DUTY

90 days of continuous active duty, called to active duty under U.S.C. Title 10. If discharged must have at least a discharge “Under Honorable Conditions”.

This includes active and retired Army, Navy, Air Force, Marines, Coast Guard, & National Guard/Reserve.

Frequently Asked Questions

-

Yes! This is not a one-time loan option. You have earned your VA Home Loan Benefit and it’s yours for life. You can reuse the benefit as many times as you want.

-

The VA funding fee is a one-time payment that the Veteran, service member, or survivor pays the VA-backed home loan program.

This fee helps to lower the cost of the loan for U.S. taxpayers since the VA home loan program does not require a down payment or monthly mortgage insurance.

If you’re required to have a funding fee, it’s financed into your loan and not paid out-of-pocket.

-

Veterans who receive VA compensation for service-connected disabilities of 10% or greater do not have to pay for a funding fee.

Veterans who would receive disability compensation if they didn’t receive retirement pay.

Veterans rated as eligible to receive compensation based on a pre-discharge exam or review.

Veterans who can but are not receiving compensation because they’re on active duty.

Purple Heart recipients.

Surviving spouses (who are not remarried) are eligible for a VA home loan.

-

Yes, lenders must calculate your student loan(s) as monthly liabilities when being qualified. However, VA is the most lenient of all programs and there are a couple different ways:

Student Loans in Forbearance: Loan balance X 5% / 12 months (ex: $5,000 loan x 5% = $250, divided by 12 months = $20.83 per month).

Student Loans on Income Based Repayment (IBR): Lender takes the contracted monthly payment on the IBR.

-

Once you own a home, VA makes it simple to refinance into a lower rate & payment or to pull up to 100% of your home’s value out.

“Streamline” Refinance (IRRRL): Refinance into a lower rate (when available) with minimal documentation and NO appraisal!

Cash-Out Refinance: Take out up to 100% of the home value for debt-consolidation, home improvements, pay for higher education and much more.